#107 - The Marina Audit: Where a Typical Yacht Club Is Leaking Value

- henry belfiori

- Apr 17

- 6 min read

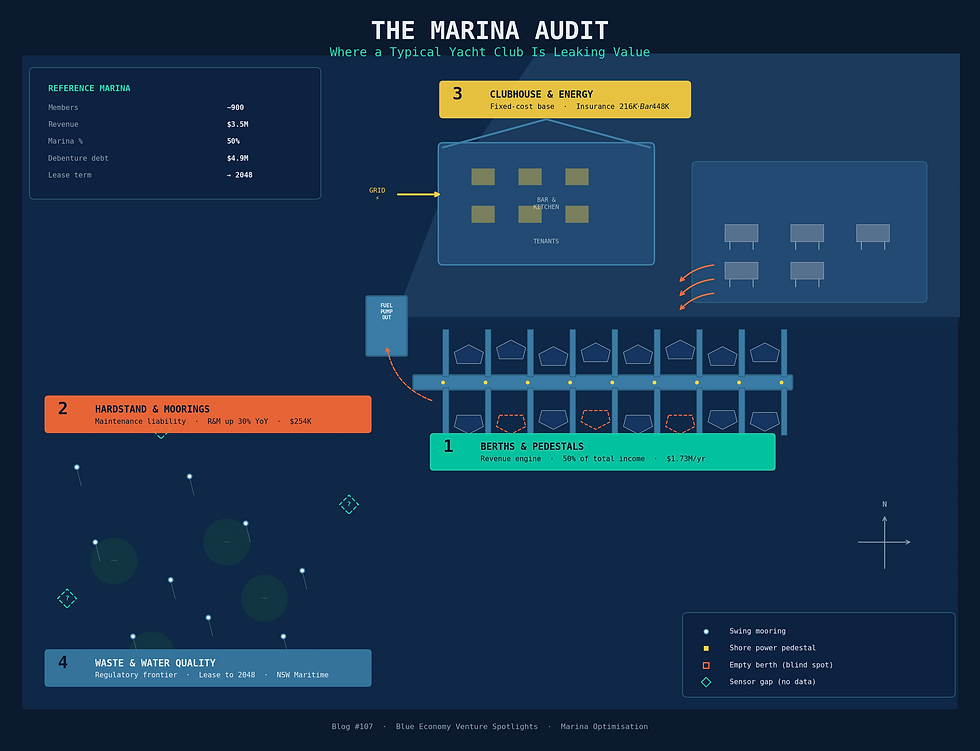

Marinas are the forgotten infrastructure edge of the Blue Economy, the physical point where recreational water users, fuel, waste, energy demand, and marine data all converge on a single site. Most are still run on paper berth plans, manual inspections, and diesel-only fuel docks. Using a mid-size Sydney yacht club (~900 members, ~$3.5M revenue) as the unnamed reference, here's a walkthrough of where the gaps are, and what kind of ventures could build into them.

Enjoy and G'day!

Zone 1: Berths & Pedestals

In our baseline marina, rentals generated $1.73M in FY2025, up 9.1% from $1.58M the prior year. This single line item accounts for 50% of total club revenue ($3.48M). Mooring rentals added $43K. Combined, water-side berth and mooring income is the business.

The problem is visibility. Most clubs of this size allocate berths via spreadsheet or paper register. There is no real-time occupancy data, no dynamic pricing for transient or visitor berths, and no way to identify underutilised capacity without a physical walkthrough.

Shore power pedestals compound this. Metering is typically aggregate (one meter per pontoon arm, not per berth). The club cannot attribute energy costs to individual vessels, which means:

No usage-based billing for shore power

No data on which berths draw peak load and when

No infrastructure readiness for EV or hybrid vessel charging

No ability to incentivise off-peak consumption

If even 5% of berth capacity is underutilised due to allocation blindness, that represents ~$86K in unrealised annual revenue at current rates. Sub-metering pedestals and billing per-berth would shift energy from a cost line to a recoverable revenue stream. A marina-ops SaaS platform that combines occupancy sensing, dynamic allocation, and utility metering is the obvious build here.

Zone 2: Hardstand, Wash-Down & Moorings

Repairs and maintenance hit $254K in FY2025, up 30.1% from $195K the prior year. Insurance ran to $216K, up 7% from $202K. These are the two fastest-growing cost lines in the operation. Both are directly connected to the physical condition of the hardstand, moorings, and hull maintenance infrastructure.

Hardstand wash-down is the environmental weak point. Antifouling paint removal generates copper and biocide-laden runoff. Most mid-size clubs have no closed-loop capture system. Water runs off the hardstand into the harbour. This is a compliance risk that tightens with every revision to state EPA and port authority discharge rules.

Swing moorings (shown on the reference layout, $43K revenue) create a different problem:

Traditional chain moorings scour the seabed. In areas with seagrass (Posidonia, Zostera), this is increasingly a regulatory trigger

Mooring inspections are manual, typically annual, done by divers. Expensive per unit and infrequent enough to miss degradation

No condition data exists between inspections

Assumptions on where efficiency sits: replacing chain moorings with elastic rode systems (e.g. Seaflex-type) eliminates seagrass scour and reduces inspection frequency. ROV or drone-based mooring inspection could cut per-unit inspection cost by 40-60% and generate a digital condition record. For the hardstand, closed-loop washdown capture with filtration is a capex item but a direct offset against rising environmental compliance costs and potentially insurance premiums. The startup archetype here is a marine maintenance-tech company selling condition monitoring hardware and packaging the compliance data for both the operator and the port authority.

Zone 3: Clubhouse, Tenants & Energy

Bar and catering revenue was $448K. Commercial rental income from tenant marine services was $403K. Together these two lines contribute $851K, roughly 24% of total revenue. Employee costs were $1.19M, flat year on year. The clubhouse is the operational hub but also the largest fixed-cost base.

Energy is unoptimised. The club runs on grid electricity with no solar, no battery storage, and no site-level energy management. Rates and utilities cost $107K in FY2025 (down from $118K, likely tariff timing rather than structural improvement). There is no disaggregated data on where energy is consumed across the site: clubhouse kitchen, bar fridges, marina lighting, tenant workshops.

Key gaps:

No rooftop solar despite a large, unshaded roof footprint on the clubhouse and hardstand buildings

No heat recovery from tenant workshop operations (grinding, welding, engine work all generate waste heat)

No shared data layer across tenants. The mechanics, riggers, and shipwrights operate independently with no visibility into each other's schedules, parts inventory, or client bookings

Insurance ($216K, up 7%) is a cost that could be influenced downward with better site-level risk data (fire monitoring, electrical load management, security systems)

Possible opportunities: a 50-80kW rooftop solar array on a site like this in Sydney would offset a meaningful share of daytime grid consumption. Payback at current NSW commercial tariffs is typically 4-6 years. The real unlock is the data layer. If the club can disaggregate energy use by zone and tenant, it can bill accurately, identify waste, and present a better risk profile to insurers. The startup archetype is a distributed energy company targeting coastal commercial sites where grid costs, insurance, and tenant density create a natural bundle.

The club's Foundation received $113K in donations and issued $88K in grants. Capital works were below plan due to contractor delays. Cash at bank closed the year at $1.02M, up from $477K. There is cash available for the right capex investment, but the board is volunteer-led and risk-averse by structure. Any vendor selling into this environment needs to lead with measurable payback, not a vision deck.

Zone 4: Waste, Sewage & Water Quality

The club holds a 32-year lease with NSW Maritime, signed December 2021, running to August 2048 at an annual rent of $151.5K (Note 3, Key Judgements). This lease is the regulatory lever. Every amendment, renewal, or compliance audit is an opportunity for the port authority to attach new conditions around discharge, water quality monitoring, and waste handling.

Pump-out facilities exist but utilisation is low across the industry. Bilge oil, plastics, food waste, and general rubbish are co-mingled. There is no separation at source and no data on waste volumes or composition.

Water quality monitoring is the biggest gap:

No continuous sensors in the marina basin or mooring field

No baseline data on turbidity, dissolved oxygen, nutrient loading, or hydrocarbon presence

No automated reporting to the port authority. Compliance is reactive (respond to incidents) rather than proactive (demonstrate ongoing performance)

The club's environmental regulation disclosure (Directors' Report, p14) states operations are "not regulated by any significant environmental regulations." This framing will age badly as state-level marine discharge rules tighten

Assumptions on where efficiency sits: continuous water quality sensors at 3-4 points across the marina and mooring field would cost $15-30K to deploy and generate a dataset that serves three audiences. The operator gets early warning on contamination events. The port authority gets automated compliance reporting. And insurers get environmental risk data that could influence premium calculations. Smart pump-out (usage tracking, automated alerts, incentivised scheduling) is a lower-tech win that improves utilisation without major capex. The startup archetype is a harbour-water-quality-as-a-service company deploying sensor networks and selling the data to operators, regulators, and insurers.

Roles: Who Has to Move

Four players sit around every marina optimisation decision. None of them can act alone.

Operator / Club Board. Controls procurement, capex approvals, and site-level strategy. At this reference club, the board includes a chartered accountant, a civil engineer, a media CEO, and a tech/education specialist (Directors' Report, p13-14). Experienced, but part-time volunteers. The Finance & Risk Committee oversees budgets. Decision cycles are slow. The board approved a debt reduction program for FY2026, which means any new capex proposal competes directly against debenture repayment ($4.9M outstanding, Note 12). Vendors need to show measurable payback within 2-3 years or they won't get through committee.

Tenant Marine Services. The mechanics, shipwrights, riggers, and sailmakers who lease workshop space on site ($403K in commercial rental income). They are closest to the daily operational pain: they see the antifoul runoff, the unmetered power draw, the ageing infrastructure. They are almost never consulted on technology decisions. Any serious marina optimisation effort that ignores the tenants will fail at implementation because they control the physical work.

Members / Boat Owners. ~900 members (collective guarantee liability of $75.2K, Note p14). They pay berth fees, bar tabs, and sailing entry fees. They drive demand signals: if members start buying EV tenders or requesting hybrid charging, the club has to respond. Member donations through the Foundation ($113K in FY2024) are a secondary funding lever. But members also vote, and member satisfaction determines whether the board keeps its seats. Any tech rollout that visibly disrupts the member experience (e.g. new access systems, changed berth allocation) needs buy-in, not just board approval.

Regulator / Port Authority. NSW Maritime controls the lease ($151.5K/yr), mooring licences, and discharge rules. This is the player most founders underestimate. The lease term runs to 2048, but conditions can be amended. The port authority doesn't need to wait for renewal to impose new water quality, waste handling, or seagrass protection requirements. Any startup building marina-tech that doesn't account for the regulatory counterparty is building on sand.

Concluding thoughts:

Marinas are an underrated Blue Economy optimisation assets. They have physical infrastructure, a captive and paying user base, predictable recurring revenue, and regulatory exposure that's already tightening on antifoul, sewage, and seagrass. The unnamed club here is carrying $4.9M in member debenture debt and running a lean operation, they're not going to adopt tech for the sake of it. What gets through the door is anything that either provably reduces a cost line (maintenance, energy, insurance) or demonstrably de-risks a regulatory obligation (discharge compliance, water quality reporting).

Super cool subject and even cool thinkign about possibilities! have a great weekend:).

OTI

H

Comments